Venture Manager Selection: Capitalising on Arbitrage Windows

Adaptability as alpha - Biotech and back again, a Hummingbird's tale - New York supremacy - and a Request for Funds

Markets age as cities do.

Communities dissolve and re-appear, windows are repaired, signs erected, and clubs bloom and fade seemingly each time you visit. Markets are similar things - ideas and money hum along in ebbs and flows around the blocs and squares of opportunity, churning out rich kids and shuttering doors just as quickly. As firms move in and out and people take on more risk to avoid competition, the windows of arbitrage open and close. Some blocs or business models are already quite efficient (e.g. marketplaces). Others have a long way to go (frontier tech).

Occasionally there are big gaps. Sometimes they’re caused by some new tech, such as the Bitcoin whitepaper or advent of cloud computing. Sometimes market changes enable them (like Constellation’s VMS strategy and the rise of LBOs in the ‘80s). Sometimes they’re crowd-brain driven (such as the 2008-2011 venture vintages), which allowed for a lot of GPs to ride the convexity inherent in low prices.

The ability to adapt to these windows of arbitrage is one of the keys we’ve seen to GP longevity. I wrote prior that the best GPs either…

“… cement themselves as the best in that sector (think Alfred Lin and SaaS) and reap the rewards of the asymmetry by virtue of their brand, or they move on to arbitrage new hunting grounds before the window closes…

Most investors struggle with the tension between this constant re-invention and dominating a space. This, I suspect, is why less than half the “good” ones stay good. They overestimate their domination and underestimate the speed at which their knowledge and networks are arbitraged.”

Hummingbird, Compound and the common thread

Anecdotally, as a no-name Belgian-origin firm, Hummingbird had to get good at looking for these windows in the early days. There was Kraken (the crypto exchange which the team put 8% of the Turkish-mandate fund into for a 16.2% stake), Peak (Turkish gaming, in a European-mandate fund), and later BillionToOne (a biotech company, from a emerging markets mandated fund).

Barend wrote about the Peak Games investment, which drove a near 9x fund-level MOIC, in retrospect that…

“Turkey was off-limits for investors. Nowadays, exceptional startups can come from anywhere. Far away from the epicenter of most tech innovation, away from FOMO, one can truly question golden rules of thumb and take the time to build a radically different culture…

Early-stage VC is often a provincial game, leaning on local networks & insider culture... Let founders benefit from global early stage insights & best practices. We crossed 10 countries to get to Turkey.”

Peak sale to Zynga drives 8.6x gross fund return for Hummingbird Ventures

The advantages of a home ground are fairly obvious: deeper relationships, easier backchanneling, off-season get-to-know-people-ahead-of-fundraising, serendipitously bumping into a prospective LP at the cafe, and so on. Any investor coming into this from the outside is at a real disadvantage. To overcome this, the investor does several things: they have local venture partners (or for larger funds, other team members covering the sector) and they have a “common thread”, something that they believe they can use to parse signal from noise better than other investors. This common thread tracks through the portfolio and often comes up when you ask a GP “why did you pick this company?”.

The common thread - in Hummingbird’s case - has been thinking deeper and more granularly about a very specific founder profile than most any other investor. The thesis is that this founder profile translates across markets and sectors enough to move in and out of them without adverse selection. For example:

“When Ileri met Atay [the founder of BillionToOne], he was struck by how different he was from other biotech founders. “I wasn’t looking at a traditional biotech company,” the investor recalled. “I was looking at a founder that possessed a lot of the traits that we were looking for.”

… The story of BillionToOne’s Series A round is a helpful case study, demonstrating Hummingbird’s process and how it resonates with founders like Atay. Hummingbird began at a disadvantage. For one thing, it was alerted of the round midway through. Given the competition to back BillionToOne, that was a real impediment. It didn’t help that Hummingbird was not exactly an expert on molecular biology.

This thread doesn’t have to be an investment belief ala Hummingbird.

It could be a process too. For instance, Compound is dictatorially thesis-driven, research-centric - it’s literally on their website. They’ve thought more deeply about how tech has inflected across a variety of liquidity cycles, markets, talent pools, adoption cycles, etc. than any other investor I’ve met.

In Compound’s case, Mike is generalist and the the rest of the team specialise in a sector. Borrowing from the USV lineage, they have weekly meetings where the team share insights, debate, and ultimately try to read various markets (eg. crypto, bio) out into the future as precisely as possible. Whether accurate or not isn’t as much the point, the thoughtful brand resonates with founders and the publicity of it gives them a flywheel a) in sectors that are hard enough already to build one in, and b) that - via investor and founder feedback - provides them with a unique meta view on the unfolding narratives.

Again, like Hummingbird, Compound moves in and out of markets trying to adapt to the competition. In 2016, Michael Dempsey wrote a post on autonomous vehicles, thinking through some of the various impacts and players. This post led to seed investments in Wayve (2017) and Runway (2018), both now worth well north of $3bn+. To quote him on this (and so give view to how he sees his common thread):

“Instead of continually jumping from new category to new category every three years, the right focus is the pursuit to be first due to a competitive advantage that first movers have within venture, and owning/exploiting that category for the next decade+ of maturation, instead of leaving it for the new, new thing after one fund (Nan Li - Defend the Hill, Scout the Frontier). There is material value in capturing the Oculus, CTRL-Labs, or Cruise’s of the world (e.g. Spark Capital invested in all 3), but in my view it’s a significantly harder moat to rely entirely on versus understanding the shifts and subsequent inflection points that result from the Oculus/Cruise/Deepminds and capitalizing on it for decades to come.”

Specialist, generalist, or New York-based

Statistically, specialist funds outperform in their first couple funds. Perhaps these funds were market-arbitraging, or perhaps the GPs were hungrier and more ambitious back then. Personally, the way I read this data is that early funds usually have an arb, and usually this arb closes.

The ability to capitalise on market windows and move on is essential. Had Hummingbird stayed in Turkey, it likely wouldn’t have generated the returns it has. Had Compound stuck exclusively with generative AI, they likely would’ve been competing for mega rounds now with Tier 1’s - outbid and outgunned by folk who’s funds and post-success psychology mandates much larger ticket sizes.

The benefits of investing in open windows are twofold:

At the deal level, better terms (the rounds are less competitive - Wayve and Runway were both sub-$10m post-money) and more time for due diligence (think of the week-long fundraises that took place during peak 2021 as a counter-example or many consensus AI rounds today).

At the company level, less consensus means bluer oceans which means less competition and more capital efficiency. Peak Games - being the first of it’s kind in Turkey - could hire all the best engineers and designers. Now, 20+ venture-backed gaming companies compete for the same talent pool in Istanbul alone. Two years back, George gave the example of African fintech:

“Once a venture-backed company achieves leadership status (several Raba companies are close) in a particular market or vertical, they have a unique position vs. peers in other markets. Because our markets are perceived as too small to support several winners, investors tend to coalesce around the market leader and the strong get stronger.”

But eventually the arb closes.

Two things happen: First, if a Fund 1 has alpha, they generally raise bigger Fund 2’s forcing them to find new and larger opportunities with the same insight. Second, other investors cotton on to the fund’s idea and begin to price it in their own opportunities or look in similar talent pools.

For example, in the early 2010’s, New York was a bit of a ghost-town venturely-speaking. It was really only Alleycorp, USV, Founder Collective, Primary, IA Ventures, betaworks, Neu and a thin handful of others passing through. The vintages for these funds at the time have done well. Like stupidly well. USV, FCVC and IA Ventures 2010-2012 vintages did >20x, the rest are all around 10x. Most of these were from sub-$100m funds, many of them invested in the same deals.2

Arguably the best decision a GP in the early 2010’s could’ve made is whether or not to HQ in New York. Now, there are 75 funds focused on the city, mostly headquartered there too, and nearly every SF fund has a strong satellite presence as well. It’s not clear that the ‘NYC arb’ has gone, but it’s certainly clear that there’s a lot more folk chasing it.

“But Jordan, LPs should not try to market-pick, it’s too blunt an instrument” Cool, yes, but nobody’s suggesting you market-pick. Going back to the specialist or generalist debate and quoting Yavuzhan:

“Being a specialist or having a deterministic conviction on a trend isn’t necessarily a positive quality. Often, we’ve seen that being a specialist is a cover for incompetency to invest at a broader scale, or giving reasons to believe for investors and LPs in the lack of any other.

We rather see value in evaluating investors together with their opportunity set, which can be generalists or specialists with different levels of granularity, to look for a bottom-up edge to allow investors to be smarter or have better access than the others. It’s possible that a domain produces multiple high-quality companies and no funds capture outlier returns if there isn’t any asymmetry of judgment and access to these companies—or it’s possible for generalist funds to capture the bulk of the value if specialists don’t have a particular edge

Top-down tailwinds don’t matter if they don’t translate into high-quality companies in investors’ portfolios with good ownership at the right prices.”

The capital stack matters

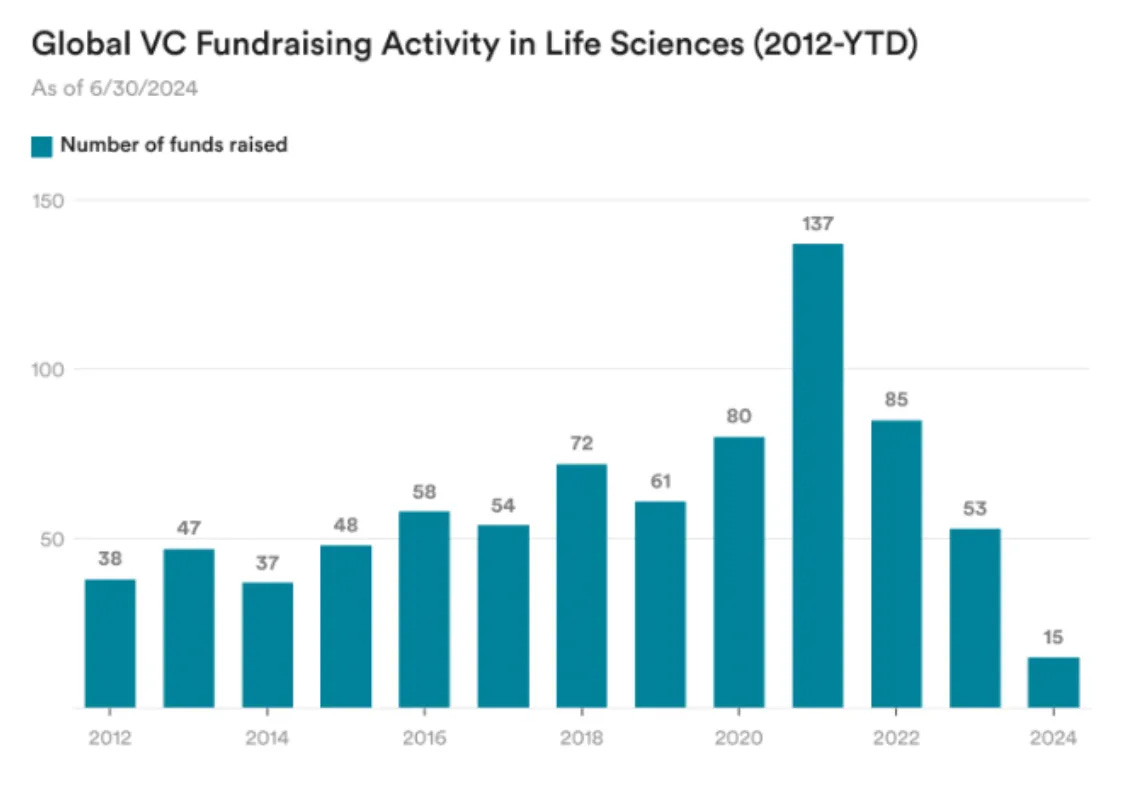

One important question to ask yourself is “where in the capital stack will the value accrue? Where - if any - are the bottlenecks?”. For instance, today even the very pedigreed life science founders can have a hard time raising. Because of the dearth of capital raised (see below), the early seed rounds get shopped around by most all the good bio funds. And this is at seed!

Outside of the mega platforms (ARCH, Third Rock, Flagship etc.) the only real name in town after Series B is Dimension. There’s a whopper of a bottleneck around them this vintage, and they’re squarely in a buyers market. This (plus the fact that they’re credible) is why so many sophisticated LPs wanted to give them money: it’s uncorrelated alpha, with a structural advantage, started by mid career investors with strong and verifiable track records prior.

For contrast, in both India and Latin America, the Series A+ market is incredibly competitive. In India, local brands like LSVP, Nexus, Peak and others are all first choice for founders. In Latin America the proximity to US and cherry-picking involvement of US players like Greenoaks, Ribbit, Sequoia and large homegrown funds like Kaszek and Monashees all make for a tough later stage market locally. In these regions, if there’s a bottleneck, it’s far more likely to be at pre-seed and seed where many founders come from less polished backgrounds (Starkbank, Tractian).

The better LPs will triangulate company level nuances between GPs to try and gauge this. For instance, if a founder speaks with every fund at pre-seed and nobody bites, then somebody bites and suddenly everyone wants in (a common occurrence in LatAm), it’s likely the value accrues to the better ‘picker’ and access isn’t weighted as highly. Alternatively, if a founder works with specific GPs early, doesn’t shop around, and the GP acts as signal for follow-on (common in SF), or there’s a well-branded program (YC, Neo, Z-fellows) that nearly everyone applies to, then sourcing and access matters a lot more.

How to find these windows

For us at Nomads, honestly this is hunch driven. After speaking with several thousand GPs and juniors from a variety of markets, you get a bit of a read of what the consensus takes are. If you look closely at their deals you can see the things that interest them now, interested them six months ago, and - if they were in venture back then - what interested them several years before that. Implicitly (and explicitly if you map it) you build up a read of where capital is flowing (informed by prices you see investors paying on a look-through basis) and where GPs expect to move next (most will tell you if you ask).

What we’re listening for from the GPs is convexity. The dream scenario would be low entry valuations (due to lack of investor interest, misunderstood founders or business models, etc.) and Big If True outcomes, with some convincible downstream buyers of our equity. The things we’re looking to avoid are steaming hot rounds, founders speed-running the venture circuit, and investing behind people who are, on average, late to well established, high status talent pools or who don’t have an ability to capture the price alpha of their being early.

That said, some markets we think sound interesting:

Applied specialised robotics (which we wrote about here from a direct perspective and here from an indirect one).

Biohacking, longevity, personalised medicine. There’s several great funds investing here (Compound, KdT, Age1, Dimension) and enough cultishness to be self-sustaining. The underlying science is increasingly trending towards real applicability and, with ever more pedigreed founders entering the talent pool, we expect there to be a temporary talent-capital mismatch.

Emerging market industrials marketplaces (Africa, Latin America). Again, there’s a bottleneck around a small handful of strong first-check investors covering these regions (Raba, CRE, OneVC). Yet there are several case studies of similar businesses playing out in India (OfBusiness, InfraMarket, Zetwerk) and in most cases (mining, chemicals, logistics, construction) the markets are large, fragmented, and are more a GTM problem. There is plenty of strong BD talent in these markets (though, admittedly, often less engineering and founder-level talent).

Indian defence, bio, and manufacturing. There’s several funds covering this now (gradCapital, Industrial47, Northpoint) but historically there’s been a huge dearth of funding with most such founders raising from US grants (1517, Emergent Ventures, Thiel, etc.) and then flying to the US before beginning to build. India is one of the few countries where defence and manufacturing have credible top-down tailwinds, and the talent density is insane. We’re beginning to see funds like Lux, Peak, LSVP etc. move in, but the appetite seems to vary by sector (for example, PopVax raised entirely from US grant funds).

Some fund-theses we think sound interesting:

Liquid-venture crypto cross-over funds. The cyclical and heavily levered nature allows for buying opportunities during down-cycles that can create venture-like returns with liquid tokens. Add to this that the crypto seed market is super well capitalised and the talent pool is pretty thin; it feels like most of the top 1% consensus pedigreed founders hoover up all the money (>$100m+ seed rounds like Monad, Blur, Ritual, and Symbiotic are far more common here than elsewhere).

AGI-centric prop-trading hedge funds. Historically, venture funds have had no business overlapping with quants, until AI. There’s a real edge some of the more frontier model acolytes can have over the Jane Streets and Citadels that’s certainly Big If True: a levered bet on the progression of AGI. Leopold Aschenbrenner is the most prolific example.

Robotics-enabled PE-style rollups of industrials. I wrote in Robotics that “In the last couple months, we’ve started to see some private equity firms targeting industrial style, low-tech, high-fragmentation, high-volume companies and using robots to automate the labour shortages.” Some examples of this include companies like Salient (a Hummingbird portfolio company), Amca (a Nomads portfolio company), and funds like Thursday.

If you’re funding companies in these areas, or thinking about starting similar funds, please reach out (twitter, linkedin).

Most academic literature holds that non-random success (skill) leads to persistence and that the random, non-persistent success is just luck. I disagree with this: it’s not necessarily that they aren’t lucky, they just lose their hunger and edge over time. If so, this means the time series analysis of returns (persistence) isn’t as indicative of skill, as the part ascribed to error or randomness is just as likely changes in alpha sources and GP motivation.

Jerry Neumann, IA Ventures, and Founder Collective all co-invested in The Trade Desk’s seed round in 2010