Indexing Venture and Other Fools' Errands

why most fund of funds aren't worth the fees - embracing nomadism - good seed investors don't compete for deals - looking for bottlenecks - and napkin art!

The point of this essay is to explain

why venture is different from other asset classes (you cannot “index” it)

why many fund-of-funds aren’t worth the fees (they try to index it)

why some fund-of-funds are (they concentrate where others don’t)

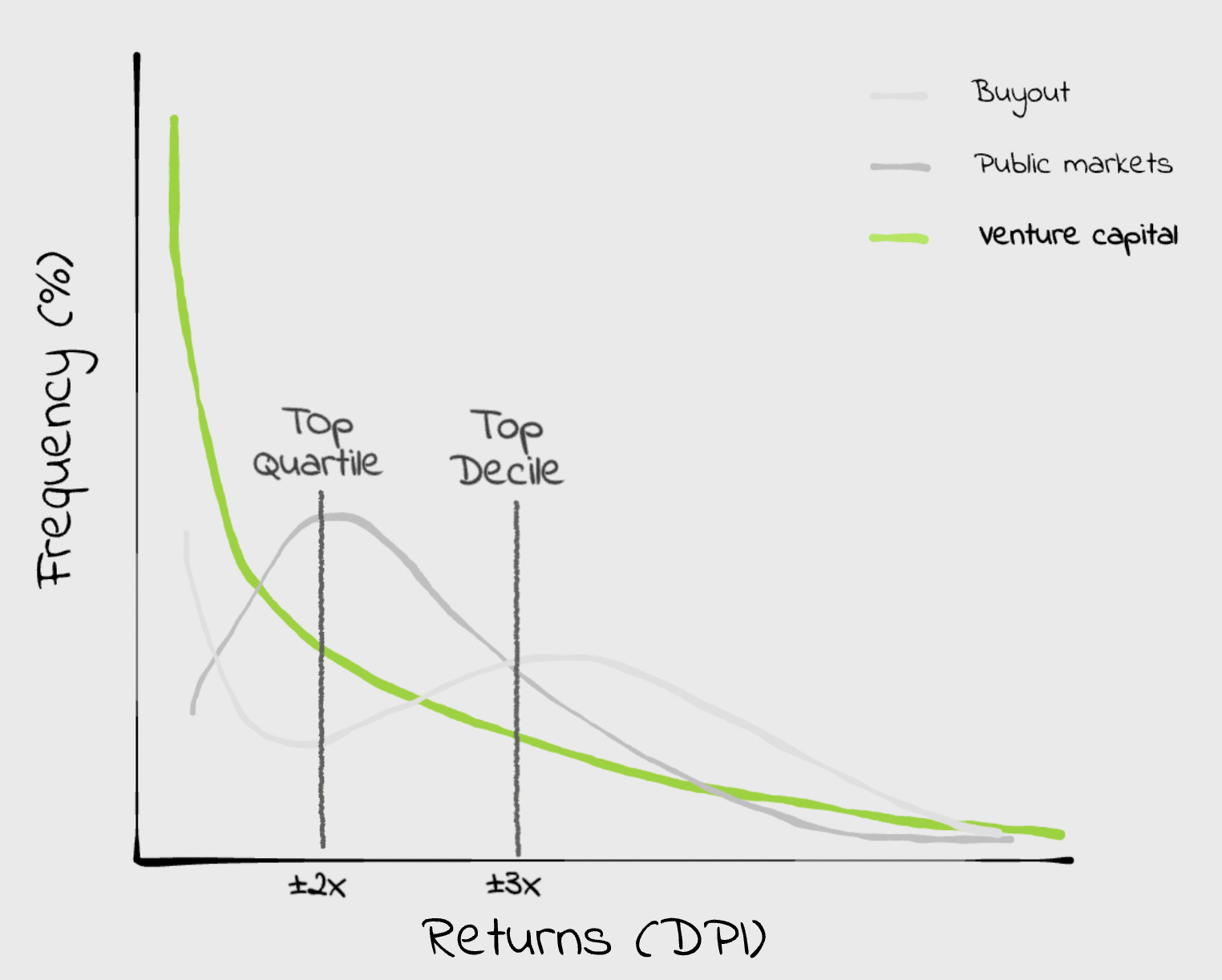

It’s a mistake to think of venture like other asset classes.

Firstly, the power law applies to both managers and their portfolios. Trying to index a power law without access to, or knowledge of, the top 1%, will leave you with very mediocre returns.1

Secondly, most attempts at indexing are done with what has worked in mind. But what has worked isn’t usually what will work. The market is too efficient and funds swell too quickly. New LPs won’t have the same asymmetry the old ones did.2

Avoiding overly efficient markets and concentrating on spaces with asymmetric upside (usually the emerging domains others aren’t investing in) is one of the few ways a fund of funds can justify their fees.

The thing that makes venture such a rough asset class is also what makes it so appealing. At the earliest stages of a company’s life the asymmetry in investing in it is the highest. Here information is murky, it is harder to distil signal from noise, networks matter more, and as prices are lower you have the most amount of upside potential.

The earlier you can source, pick, and win a great founder over, the better your returns will be. But everyone else is trying to do the same. Usually you have to see something they don’t in either the product, market, or person. This is how the best seed funds differentiate themselves - they pick differently.

The gap to do this is not long-lasting. The window of arbitrage opens and closes as firms move in and out and folk take on different risk profiles to avoid the competition. Some sectors (such as neobanks and consumer marketplaces) have lost a lot of the arbitrage in the last decade. Big funds have come earlier and applied a standard-higher pricing, the number of GPs have increased, and folk know what underwriting lens to apply. I wrote about this in a previous essay.

These dynamics - the asymmetry of the early stage and arbitrage of different picking - are what many of the top 1% of investors capitalise on. Either they cement themselves as the best in that sector (think Alfred Lin and SaaS) and reap the rewards of the asymmetry by virtue of their brand, or they move on to arbitrage new hunting grounds before the window closes. Sometimes it’s a mix of both. Either way, the best seed investors don’t really compete for deals.3

Most investors struggle with the tension between this constant re-invention and dominating a space. This, I suspect, is why less than half the “good” ones stay good. They overestimate their domination and underestimate the speed at which their knowledge and networks are arbitraged. It is easy to tell yourself, as prices creep up, that “venture is still asymmetric, this is just the market as it is, my LPs pay me to deploy”.

The math gets really hard really quickly. As prices rise, a fund’s portfolio moves from convex (unbounded upside, bounded downside) closer to a concave profile (trimmed upside given the opportunity is priced in at entry valuations).

This, I also suspect, is why it’s nearly impossible to index venture. Most funds can’t capitalise on the asymmetry to begin with. Those who can, usually only do it for one or two vintages. If a fund manages to do well over multiple cycles, they inevitably become access constrained and out of reach for most LPs.

So most LPs are forced to try index the top quartile funds. They don’t know what it looks like to pick differently, and so need to rely on track records and brand to judge funds. Only looking at what has worked will almost never get you into funds above top quartile. Because of that, most people will continue to lose money in venture.4

Most fund-of-funds can’t justify the fees they charge.

They’re expensive, too diversified to capitalise on great funds, and anchor their value prop around diversification and/or access. Most are ossified, have no underwriting edge of their own, don’t have real access and invest through the rear-view mirror. If your goal is a diversified spread of top quartile funds, then you may not know it but you’re trying to index venture.

If you are adversely selected out of the well-known high-performing funds and you can’t pick the right lesser-known ones, then your diversification is worse than market beta. Say you take a public market index, for example the S&P 500, and you remove the 7 best performers, you net nearly zero year to date. Venture is far, far more power law than the public market - removing the top performers removes almost all the performance.

So what do you do to try and find the outliers?

You get nomadic. The top performing funds of a vintage are not usually the brand names you know. Outlier funds are, by definition, outliers: they don’t look the same as the other ones. Most change with each cycle and - given their small fund sizes5 and different approaches - they are often hard to spot and even harder to size. In some ways, it takes one to know one.

In every cycle there are GPs who perfectly time inflection points of emerging domains, propelling them to the top 1% of that vintage. USV did this with the social graph, Paradigm and crypto, Ribbit and fintech and so on.

Founders building in these domains are often fringe folk (think, early crypto), the business models are unusual (the social graph), or the market is quite tough to understand and has a lot of quirks to get over (usually this is geographic). These traits act as a barrier to investors and create a bottleneck around those investing there.

A fund of funds that can find investors arbitraging these bottlenecks can act as a guide to the domain for less familiar LPs. Looking in places where there’s not much capital to begin with also means the fund can act as valuable downstream capital for its GP partners. This set up is part of whats make a good fund of funds, with reasonably concentrated and selective picking, statistically more likely to be a high returner than a good single fund of similar diversification.6

So why don’t we see more FOFs putting up these numbers? Well, some do. But most continue to index. They are happy to re-up in the same funds, go on skiing holidays, and tell their rich friends that they’re “venture capitalists”.

I’m obviously talking my book here. In this industry it’s healthy to be skeptical of anyone not talking their book. At Nomads we want to be meaningful partners to the best early stage managers. We have a concentrated approach and focus on emerging domains (currently, Africa, India, SEA, techbio, and robotics). Please reach out if you’re thinking about leaving a large fund, starting your own fund, or are an aspiring angel in an interesting domain.

Tomer wrote a good article on the portfolio math for TechCrunch

AUM is the equilibrium lever in venture, not price.

The basics of an efficient market are that prices reflect scarcity value. So someone with a well oversubscribed fund should raise their prices even more to find equilibrium. But they don’t as there’s a social compact around fee range and their net returns would drop. When a fund prioritises net returns they accept that they’re giving up surplus value.

New players enter the market and funds with less care for returns swell to accommodate investor interest. In commoditised sectors returns usually accrue to the investor with the lowest cost of capital and who’s LPs are willing to take on the lowest assured IRR (this is the strategy behind most multi-billion dollar funds)

Thanks Sam

The median fund return is 1x and most (!) managers underperform the S&P 500. Cowboy investing has a great article on retail investors losing money

“Fund size is not a magical number that is important in isolation. It’s just an independent variable that determines some key dependent variables like the number of companies in the portfolio, entry valuation-ownership, and available follow-on reserves.” - Yavuzhan, A guide to size in venture funds