Allocator’s Notebook: Version One Funds I-IV

Funds to study - arb windows (again) - Bay Area benchmarks - you can miss Shopify and still have an outlier fund

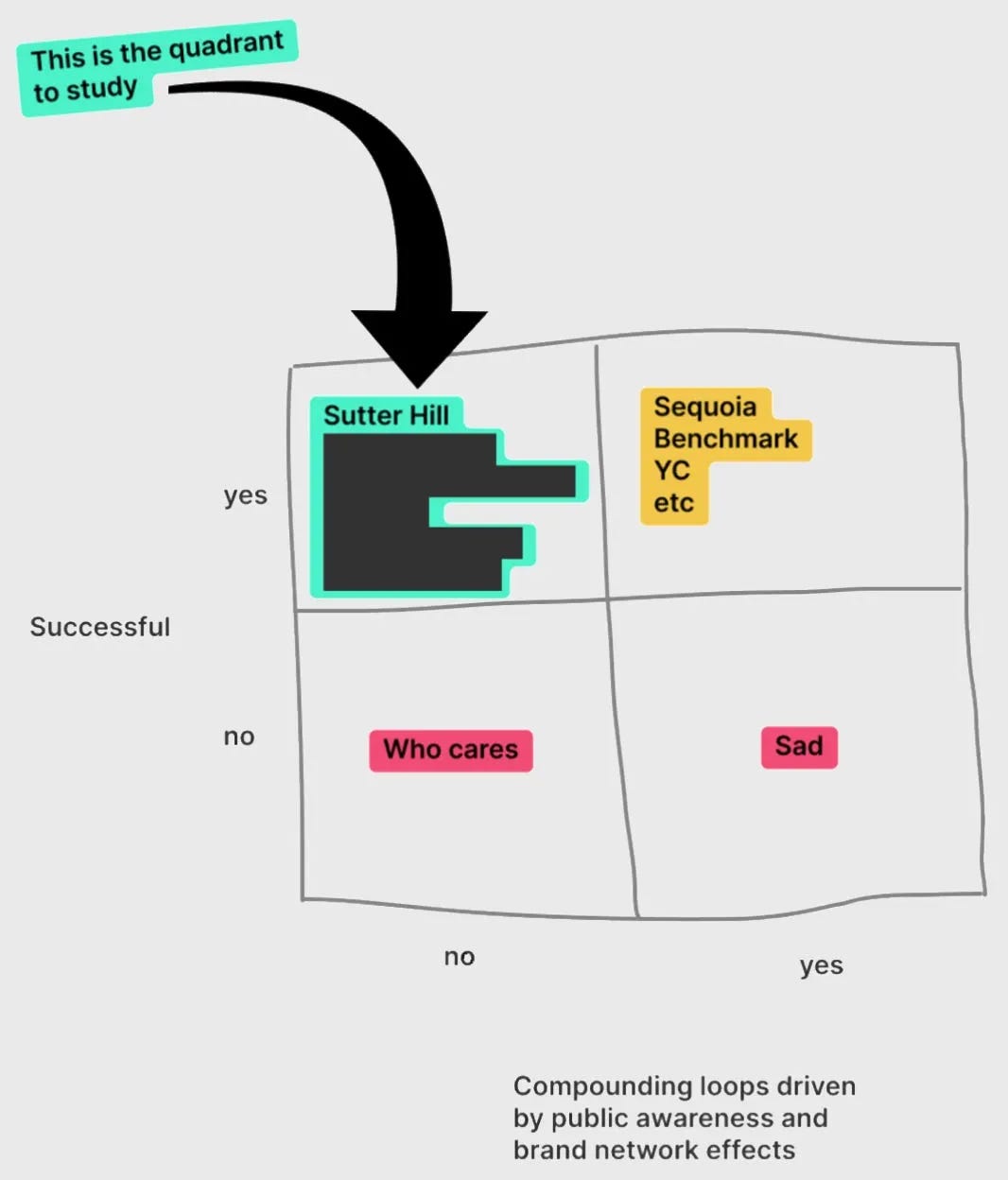

Kevin Kwok’s funds-to-study graphic from his piece on Mike Speiser is one of my all time favourites. One of our aims with this Allocator’s Notebook series is to understand the funds in this quadrant.1

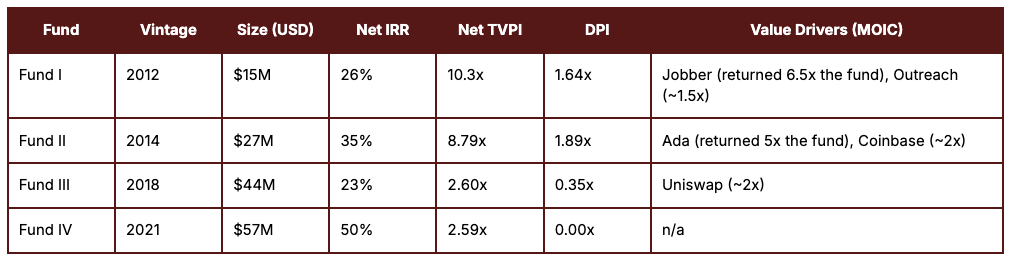

Version One is such a fund. Funds I and II both sitting at 8.79x and 10.3x TVPI as of today with value drivers coming from vertical SaaS and crypto. Starting out in Canadian marketplaces, now they’re making investments in India, bio, deep tech, even other fund managers.

I wrote in Venture Manager Selection: Capitalising on Arbitrage Windows that:

“Markets age as cities do.

Communities dissolve and re-appear, windows are repaired, signs erected, and clubs bloom and fade seemingly each time you visit. Markets are similar things - ideas and money hum along in ebbs and flows around the blocs and squares of opportunity, churning out rich kids and shuttering doors just as quickly. As firms move in and out and people take on more risk to avoid competition, the windows of arbitrage open and close. Some blocs or business models are already quite efficient (e.g. marketplaces). Others have a long way to go (frontier tech).”

I didn’t know it then but near verbatim this is Boris and Angela’s philosophy.

History

As a kid and throughout college (he finished his PhD and grad studies at Otto Beisheim School of Management), Boris grew snails for eating (an unsuccessful venture), started a consulting company (again unsuccessful), and imported North American cars to Europe before founding JustBooks.de in 1999 (which found some success). JustBooks was acquired by AbeBooks in 2002, which Boris co-led as COO until its $110M sale to Amazon in 2008. Post-exit, he made ~30 angel investments from 2008-2012, before launching Version One and serving as a board partner of a16z from 2014-2021.

He raised Version One Fund I in 2012 as the sole GP from a handful of American-Canadian exited founders and tech execs (including Yahoo president and COO Jeff Mallett). He built the firm from Vancouver, without a Bay Area presence during Funds I-II.

Angela Tran joined as an analyst in 2013 (becoming GP in 2018). She moved to the Bay Area in 2010, then defended her doctorate in applied science at the University of Toronto and co-founded YC-backed Insight Data Science in 2012. The team has remained small, adding CFO Leah Gosbee later.

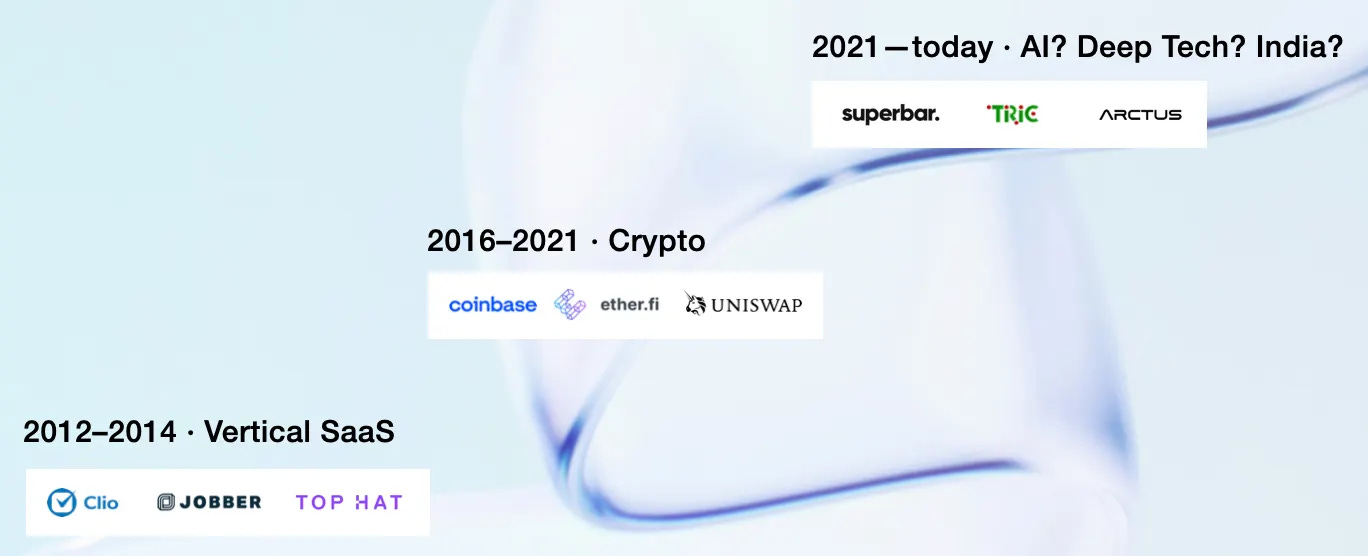

The First Act of Version One were SaaS and marketplaces between 2012 and 2015. They wrote a Marketplace Handbook, invested in companies like Jobber, Clio and Ada - all Canadians, all business models and markets Boris knew well, and all had near-death experiences early on. Between 2016 and 2018, both Boris and Angela said numerous times that the marketplace investing had become too crowded. They made no new marketplace investments after May 2015 (despite writing about marketplaces and speaking at marketplace events until recently).

The Second Act of Version One was crypto. Between 2015 and 2021 they backed Coinbase, Uniswap, EtherFi, and Dapper Labs. They would use the marketplace lens (liquidity, chicken-egg problem, take rate, network effects, etc.) and apply it to crypto primitives (DEXes, NFT platforms, staking derivatives, mutuals).

The Third Act of Version One - the one you’re likely to meet if you speak to the team today - is massively exploratory. Boris has been personally LP’ing into other funds since 2013 and the team have made many direct investments into India, deep tech, healthcare and vertical AI off the back of these nodes.2

Key Companies

Jobber: Version One led the first couple rounds (2012, 2014, Fund I) alongside Point Nine.

Sam Pillar (30*) and Forrest Zeisler (29*) were University of Alberta grads and freelance developers who founded Jobber in 2011 as a business management platform for home service businesses (landscapers, domestic services etc.).

Jobber reached ~$1.25B valuation by 2024, delivering 135x return (29x realised via secondary sales in 2017 and 2023). The company has since raised ~$183M from General Atlantic and others. Version One’s stake implied ~6.5x the $15M Fund I.

Jobber was the first investment from Boris’ first institutional fund, and he has stayed on the board of the company since then. Convinced of the “insane focus of the team on product and creating value for customers” and seeing the rapid commercialisation of new features, both Version One and Point Nine bridged the company several times during the non-consensus period between the first seed investment (2012) and the $8M Series A (2015). The most common push-back from investors during that time was that the product was too niche and not building in a clear category, and that the team was based in Edmonton, Alberta.

* Age at the time of the Version One investment

Outreach: Version One participated in the pre-seed round (2013, Fund I).

Manny Medina (40*) was a repeat immigrant founder of middling success who prior led BD for Microsoft’s Canadian and Latin American arms.

Outreach hit $1.96B** valuation by 2024, yielding 65x. Version One’s position was ~1.5x Fund I.

The 4 co-founders initially met in TechStars in 2011, launched an hiring marketplace which struggled and, with two months of runway left, pivoted on Boris’ advice to selling an internal email tool they’d developed. They rebranded as Outreach (Boris and another investor bridged with $150k total) and spent two years raising from angels and growing the sales team.

They raised a $2.3M round (in which Boris and Floodgate participated) and went from almost bankrupt to $10M in ARR in 2 years, finding success selling SaaS to help sales reps manage their pipeline.

* Age at the time of the Version One investment

** Version One internal marks

Ada: Version One led the pre-seed round of Mike and David’s prior company and participated the $2.8M USD seed round post-pivot (November 2016, Fund II).

Mike Murchison (28*) and David Hariri (27*) had previously co-founded Volley together, a social search community for feedback on niche challenges, both two years out of college - Boris and Angela had previously led Volley’s pre-seed round. Both founders are Canadian, with Mike also having founded several prior startups during and after college.

Ada reached $909M** USD valuation by 2024, delivering 48× return. The company has since raised ~$200M from Accel, Tiger, Spark, First Mark and Bessemer and Version One’s early position is held at ~5× the $35M Fund II.

The founders decided to wind down Volley and pivot to Ada - a pivot from a social network to SaaS, customer support chatbot - with early customers Medium, Kik and Wattpad (a prior portfolio company of Boris’). The team raised a $2.8M seed from Bessemer in late 2016 (in which Boris and Angela doubled down) and found real traction selling to Coinbase and Shopify.

* Age at the time of the Version One investment

** Version One internal marks

Coinbase: Version One joined Series D and E ($2M investment combined, 2017, 2018, Fund II).

Brian Armstrong (34*) was an Airbnb engineer; Fred Ehrsam (29*) a Goldman trader. They had raised previously from Y Combinator (Seed, 2012), Union Square Ventures (Series A, 2013), Andreessen Horowitz (Series B, 2013), and DFJ Growth (Series C, 2015).

The Series D was $100M at $1.6B led by IVP. Version one participated alongside Spark, Greylock, Battery, Draper and others. It was the largest tradfi funding crypto had seen - a highly competitive round given the explosive user growth Coinbase was seeing amidst the broader ICO craze. Coinbase IPO’d in 2021 at $85B; Version One realised 24.6x. Their stake was worth ~$50M, ~1.4x the $35M Fund II.

Boris justified the exception to their seed mandate at the time by (correctly) seeing Coinbase as the clear category leader, with high moats, in an sector they’d had a public thesis on since 2016.

* Age at the time of the Version One investment

Learnings

As in the USV and Ribbit stories, it is never too late to start an outlier fund. Boris was 39 years old when he started Version One, with an operator-angel background, without any institutional-grade investment track record.

It’s not obvious which companies will ultimately be the value drivers. Jobber, Ada, Outreach all pivoted or had near-death moments and all were non-consensus deals building outside of Silicon Valley. None of the companies Boris was excited about as an angel - Indiegogo (acq. in 2025 at ~40m revenue), Flurry (acq by Yahoo in 2014 for ~200-300m), Wattpad (acq. for $600m in 2021) - ultimately had generational type outcomes. In 2013, his biggest regret-pass was HootSuite (valued <$1bn today)

Having Bay Area benchmarks for talent is often an edge over local-only investors. In the early days (in interviews with a16z, Startup Grind Vancouver and at GROW 2013) Boris often compared local scenes to SF, contrasting founder profiles, capital and mentorship availability, early hires, and level of ambition. Boris would fly to SF monthly spending weeks on end there, and Angela has been based there since 2010.

Optically, the team is playing a ‘value’ game. Unlike Ribbit and USV - who’s early outperformance came from picking (and paying for) premium - Version One’s was baked into the convexity of their small fund and low entry prices approach. There’s an idea that “There isn’t a secondary market, there’s a list of 20 companies with infinite demand for their equity.” As Version One have yet to invest early into a $10B dollar company, this value approach might explain the TVPI-DPI difference. Alternatively, that the team recently bought secondaries in both Jobber and Headout could also explain the difference.

Like NYC based USV and Compound, publicly sharing theses in a granular way helped them win access to competitive rounds. Coinbase COO Emilie Choi said they wanted Version One in given crypto is a cyclical industry and the team had a “very specific thesis on blockchain and crypto” to help them bear through the winters. The marketplace handbook Boris and Angela wrote was shared by a16z and revised several times between 2015-2018.

They actively moved out of closing arb windows. By the time their marketplace handbook was revised (including all the mentions to Redpoint, P9, USV, Benchmark and a near dozen other funds who were writing posts about marketplaces), Boris and Angela had moved on to crypto.

Reflecting on their fund journey: “In the early years (Funds I and II), we saw more value created from every dollar we invested in Canada compared to the US. For instance, in Fund I, every dollar invested in Canada generated $12 in value, while in the US, it created $7. However, as our focus has evolved, so has the geographic distribution of value creation. By the time we reached Fund III, the dynamics shifted. A dollar invested in Canada generates $2.30, while in the US, it yields $3, and internationally, it generates $9.10”

The team were intentional about acting as signal to big funds. Boris mentions being known as the link between Canadian entrepreneurs and the US funds, and while he was a board partner of a16z he would rope them into deals. Bessemer marked Boris and Angela up on Ada; it was a young Ben Mathews (at the time at BVP, now runs Night Ventures) who first sourced Mike and David through Volley’s mobile social app, introducing them to Boris and Angela to lead the pre-seed.

Their investment decisions are nearly entirely team-driven. Twelve years ago, when starting V1 and reflecting on his angel career, Boris mentioned that “[He] always thought it was probably 50 percent traction, 50 percent team, and today [he] think[s] in the early stages it is 98 percent team, and traction is just a reflection of how good that team is.” How does he assess this? Often by using market-traction questions to gauge the level of obsessiveness of a team, saying:“… once you reach some scale, like somebody that has a startup and does not know what his churn rate is, what his sign-up rates are, et cetera - somebody that runs a marketplace and does not have his cohort analysis with him - it is just usually an expression of not caring about the details and not wanting to use data to really understand where you can prioritize the most scarce resource you have, which is your time”

You can miss the big winners in your scope and still have an outlier fund if the mathematics are right. Despite being in Canada, they never invested in Shopify. In 2014, Boris mentioned actively building a thesis around hardware companies and around companies selling to government yet missed out on Anduril (an instance where being in the right network matters more than having the right thesis). They also passed on Instacart post-YC in 2012 despite it being a marketplace and having conviction in Apoorva Mehta.

Actively changing investment behaviour after realising errors shows flexibility. In 2011 they looked at the Series B of Shopify (then valued at $100M). One imagines they must’ve referred back to this painful pass as Shopify was worth ~$3.5B publicly when they underwrote Coinbase’ Series D, and gained conviction in making the later stage exception. In another example, Boris passed on Clio as an angel and later invested in the Series C alongside Point Nine.

There were early wrinklings of a highly exploratory mindset in Fund I. Boris was known as nomadic, being ‘everywhere all the time’ and his answer in 2013 to a student who asked for advice was “[Deal flow] is usually a thing that develops over time. In the beginning, you only invest locally, then you expand your reach, you invest in Seattle and perhaps Western Canada, and over time you get broader.” I imagine early LPs would’ve heard this and thought that they are not betting on a Canadian specialist but rather a global generalist.

Emerging managers often move in a group. In addition to the Point Nine overlaps (Clio, Jobber), Fred Wilson of USV also makes reference to collaborating with Boris, hiring someone for him. Boris took a close look at Honey’s $500K round at a $12M valuation in 2015 (the same round that drove Mucker Capital’s 30x Fund I). He met Henry Ward (founder of Carta) via Manu Kumar from K9 Ventures in 2013. Boris passed, but Manu invested from a fund that went on to do 40x.

Resources

More reading!

Version One Blog, January 2013: Jobber Investment Announcement

YouTube, August 16, 2013: “Interview with Boris Wertz at GROW 2013 in Vancouver”

a16z Blog, April 30, 2014: “The Nomad VC: a16z’s Newest Board Partner Boris Wertz”

BCBusiness, February 4, 2010: “The Second Life of Boris Wertz”

Venture Capital Journal, December 20, 2016: “5 Qs with Boris Wertz, GP of Version One Ventures”

YouTube, August 30, 2013: “Boris Wertz (Version One Ventures) at Startup Grind Vancouver”

Business in Vancouver, July 22, 2013: “How I did it: Boris Wertz”

Version One Blog, March 20, 2019: “Where is the value in tokens?” (early crypto thesis reflection)

Inside Outreach: The Hard-Charging Cloud Startup Thriving In Salesforce’s Shadow

How A Kid Who Sold Snails Grew Up To Be A Successful Entrepreneur, Then Angel Investor